Power of Vega in Options Trading

This post is about an important Option Greek: Vega. Option Greeks are vital tools for options traders, enabling them to gain deeper insights into their options positions and make more informed decisions. In this post, we'll break down what Vega is, why it matters, and how you can calculate it and use it for trading options.

All the concepts covered in this post are taken from the Quantra course on Options Volatility Trading: Concepts and Strategies. You can preview the concepts taught in this course by clicking on the free preview button and going to the Section 17 and Unit 16 of the course.

Note: The links in this tutorial will be accessible only after logging into quantra.quantinsti.com

What Is Vega and Why Is It Important?

In simple terms, Vega represents an option's sensitivity to changes in the implied volatility of the underlying asset. Implied volatility is a measure of the market's expectations for future price fluctuations. Vega measures how much an option's price is expected to change for a 1% change in implied volatility.

Vega is important because it helps traders assess the impact of volatility changes on their options positions. When implied volatility increases, options tend to become more expensive, and vice versa. Traders can use Vega to anticipate how their options might be affected by changes in market volatility and adjust their strategies accordingly.

How does Vega behave for call and put options?

Vega behaves similarly for both call options and put options. In general, Vega measures an option's sensitivity to changes in implied volatility, and it doesn't depend on the option being a call or a put.

Here's how Vega typically behaves for options:

- Positive Vega: The option's price is expected to increase when implied volatility rises and decrease when implied volatility falls. When traders say an option is "long Vega," it means the option benefits from an increase in volatility.

- Negative Vega: Conversely, when implied volatility decreases, the price of call options tends to decrease, resulting in a negative impact on the option's value. Options that are "short Vega" may experience losses when volatility decreases.

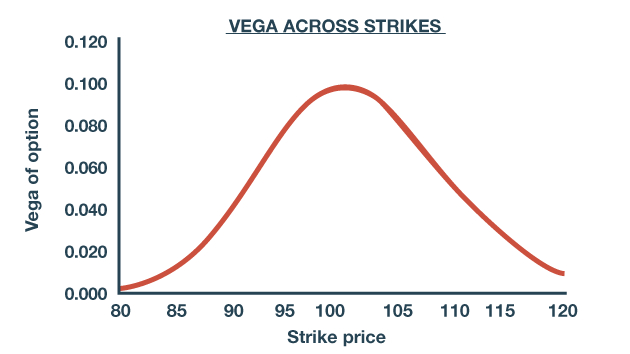

How does Vega change across strikes?

While Vega is generally similar for call and put options, it can vary across different strike prices. At-the-money options typically have higher Vega compared to in-the-money or out-of-the-money options.

For example, if the ATM strike price is $100 then the vega will be maximum for $100 option as shown in the graph below:

How to calculate Vega?

Vega can be calculated using the following formula:

Vega = Change in Option Price / Change in Implied Volatility

Let's illustrate this with an example:

Suppose the $100 strike call option has an IV of 30%, and the option price is $5. When the IV of the stock XYZ changes from 30% to 35%, then the $100 strike call price changes from $5 to $5.5. What is the vega of this option?

Vega = Change in Option Price / Change in Implied Volatility

Vega = ($5.5 - $5) / (0.35 - 0.3)

Vega = 10

In this way, you can calculate the Vega of any option. However, doing this manually for every option can be a tedious process. You can use the mibian Python library to programmatically compute Vega of any option.

For example:

# Import library

import mibian

# Define parameters for the options contract

stock_price = 100

strike_price = 100

interest_rate = 0

days_to_expiry = 40

volatility = 30

# Compute vega

vega = mibian.BS([stock_price, strike_price, interest_rate, days_to_expiry], volatility=volatility).vega

# Print vega value

print(vega)

The values of the parameters taken above are for illustrative purposes only. You can change the values as per your options contract.

How Traders Use Vega?

Traders use Vega as a key metric in options trading to assess and manage the impact of changes in implied volatility on their options positions. Changes in implied volatility, driven by shifts in market sentiment or events affecting the option's underlying asset, have a more significant impact on Vega.

For example, prior to an anticipated earnings announcement or a major economic event, market participants often expect increased volatility as uncertainty rises, which results in higher Vega values for options. This expectation of heightened volatility causes an increase in implied volatility. One way to trade this heightened volatility is by deploying a short straddle to capture the volatility reduction. We have discussed the short straddle strategy in detail here.

Nevertheless, prior to implementing any trading strategy, it is crucial to conduct a thorough backtest. This process allows for an evaluation of the strategy's effectiveness, providing insights into its historical performance.

The backtesting of the short straddle strategy has been covered in detail along with the Python code in this unit of the Options Volatility Trading: Concepts and Strategies course. You need to take a Free Preview of the course by clicking on the green-coloured Free Preview button on the right corner of the screen next to the FAQs tab and go to Section 17 and Unit 16 of the course.

What to do next?

- Go to this course

- Click on

- Go through 10-15% of course content

Drop us your comments and queries on the community

IMPORTANT DISCLAIMER: This post is for educational purposes only and is not a solicitation or recommendation to buy or sell any securities. Investing in financial markets involves risks and you should seek the advice of a licensed financial advisor before making any investment decisions. Your investment decisions are solely your responsibility. The information provided is based on publicly available data and our own analysis, and we do not guarantee its accuracy or completeness. By no means is this communication sent as the licensed equity analysts or financial advisors and it should not be construed as professional advice or a recommendation to buy or sell any securities or any other kind of asset.