Backtesting Options Strategy: Short Straddle

In this post, we will talk about an options trading strategy: Short Straddle.

In a short straddle, traders sell both a call option and a put option with the same strike price and expiration date, anticipating a reduction in implied volatility. The goal is to profit from the time decay of options premiums as both the call and put options erode in value. This strategy can be applied to all "European Type" options.

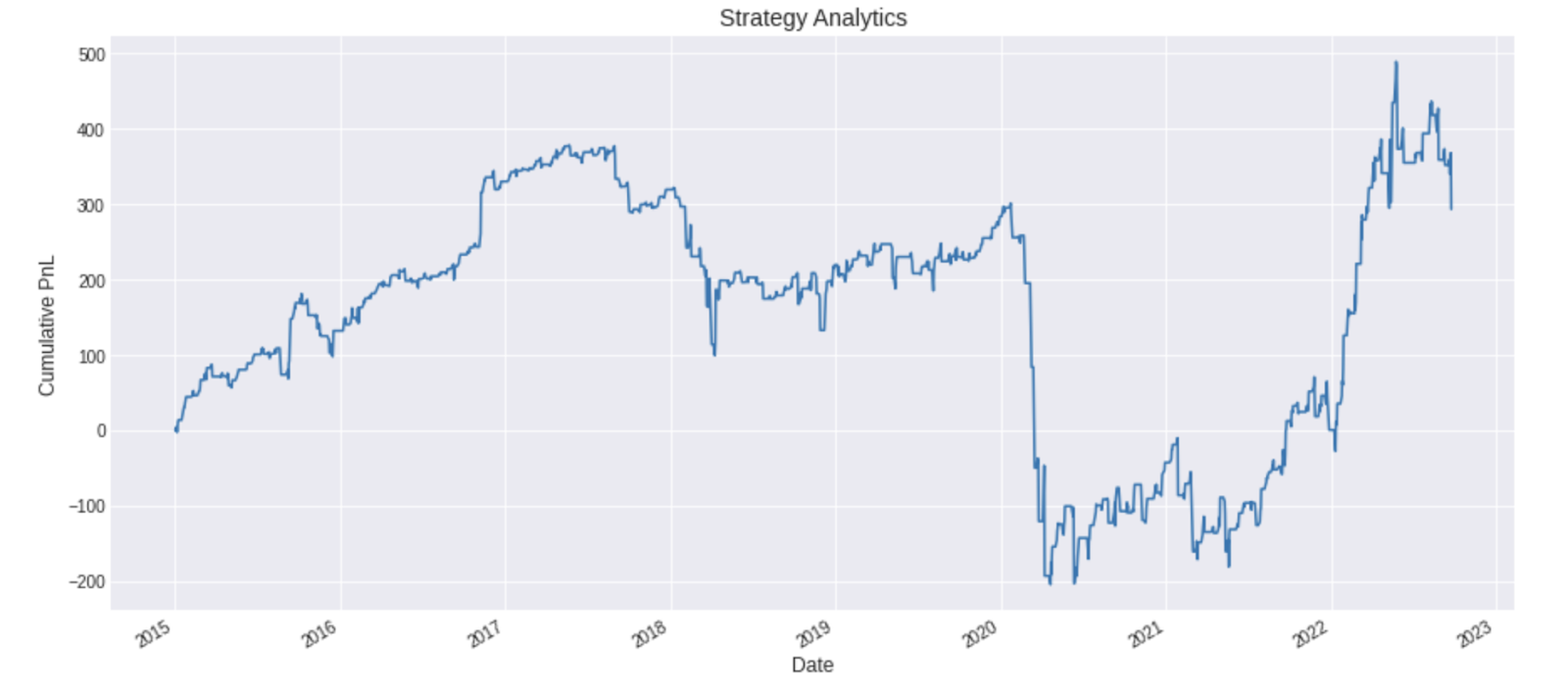

We backtested a variation of the short straddle strategy on SPX options over a period of 8 years, and these were the results:

Performance Plot

It is important to note that backtesting results do not guarantee future performance. The presented strategy results are intended solely for educational purposes and should not be interpreted as investment advice. A comprehensive evaluation of the strategy across multiple parameters is necessary to assess its effectiveness.

All the concepts covered in this post, are taken from the Quantra course on Options Volatility Trading: Concepts and Strategies. You can preview the concepts taught in this course by clicking on the free preview button and going to Section 17 and Unit 16 of the course.

Note: The links in this tutorial will be accessible only after logging into quantra.quantinsti.com

What is the short straddle strategy?

The short straddle is an options trading strategy where a trader sells both a call option and a put option with the same strike price and expiration date. Here's a breakdown of the components of a short straddle:

- Selling Call Option: The trader sells a call option, giving the buyer the right to purchase the underlying asset at a specified strike price before the option's expiration date.

- Selling Put Option: Simultaneously, the trader sells a put option, granting the buyer the right to sell the underlying asset at the same strike price before the option's expiration.

Both the call and put options involved in a short straddle have the same strike price and expiration date. This creates a "straddle" because the trader is positioned on both sides of the market.

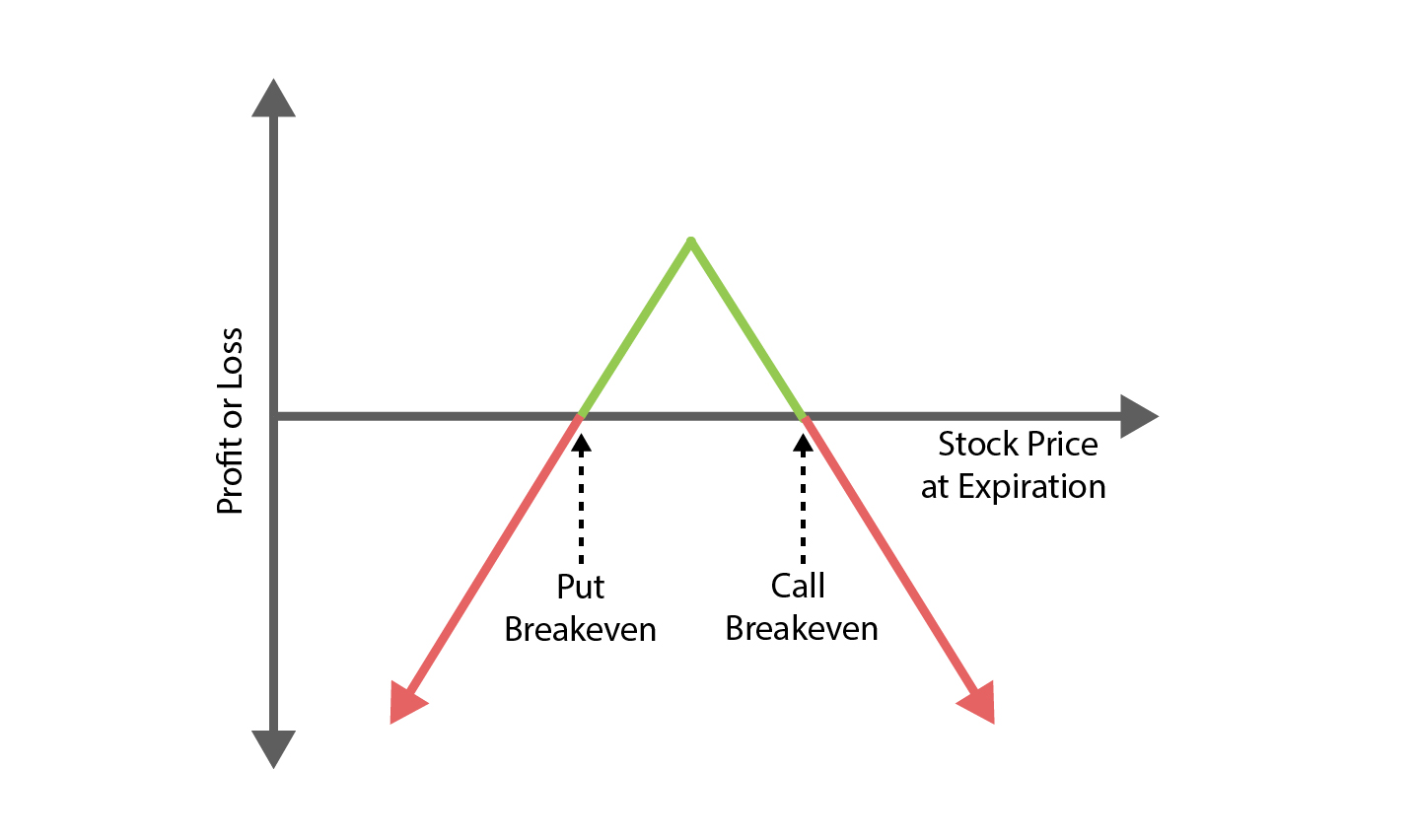

What is the risk and profit potential when trading a short straddle?

The maximum profit for a short straddle is the combined premiums received from selling the call and put options. However, the risk is theoretically unlimited because the underlying asset's price can move significantly in either direction. That is why it is very important to have a proper stop-loss in place while trading a short straddle.

Short Straddle Payoff

When can you trade a short straddle?

You can trade a short straddle when you anticipate a reduction in implied volatility. The strategy profits the most when the market price remains close to the strike price until the options expire, allowing both the call and put options to expire worthless.

What is the volatility premium?

The volatility premium (also known as variance premium) is the difference between implied volatility (expectation) and realised volatility (actual). If implied volatility is higher than realised volatility, there is said to be a positive variance premium. Conversely, if implied volatility is lower than realised volatility, there is a negative variance premium.

What is the significance of volatility premium?

At its core, the variance premium signifies that options are typically overvalued in the market. It is a phenomenon where the implied volatility (expectation) of options tends to be higher than the subsequent realised volatility (actual). In simpler terms, there's a trading opportunity by selling options without engaging in complex strategies. For example, selling a straddle can result in profits from high implied volatility as the market tends to overestimate the potential price movement.

We backtested this strategy on SPX options, and these were the results:

Performance Plot

So, in this post, we discussed the short straddle strategy and how we can harvest the variance premium by deploying a short straddle. You can easily backtest the short straddle strategy discussed above using Python code.

It is important to note that backtesting results do not guarantee future performance. The presented strategy results are intended solely for educational purposes and should not be interpreted as investment advice. A comprehensive evaluation of the strategy across multiple parameters is necessary to assess its effectiveness.

All you have to do is take a free preview of this unit of the Options Volatility Trading: Concepts and Strategies course. To take a free preview you need to click on the green-coloured Free Preview button on the right corner of the screen next to the FAQs tab and go to Section 17 and Unit 16 of the course.

What to do next?

- Go to this course

- Click on

- Go through 10-15% of course content

- Drop us your comments and queries on the community

The course "Options Volatility Trading: Concepts and Strategies" is co-authored by Dr. Euan Sinclair, who possesses over 27 years of experience in the industry and has authored three books on options: "Options Trading," "Volatility Trading," and "Positional Options Trading"

IMPORTANT DISCLAIMER: This post is for educational purposes only and is not a solicitation or recommendation to buy or sell any securities. Investing in financial markets involves risks and you should seek the advice of a licensed financial advisor before making any investment decisions. Your investment decisions are solely your responsibility. The information provided is based on publicly available data and our own analysis, and we do not guarantee its accuracy or completeness. By no means is this communication sent as the licensed equity analysts or financial advisors and it should not be construed as professional advice or a recommendation to buy or sell any securities or any other kind of asset.