Trading With Gamma

Have you ever wondered which options strategy professional traders deploy in volatile or uncertain markets? One of the key techniques they use is gamma scalping. This method allows traders to dynamically adjust their positions to profit from market movements while mitigating risks. In this post, we'll explore the concept of gamma in options trading, explore what gamma scalping is, and discuss how it can be applied in the market with the help of a practical example.

Let’s get started!

All the concepts covered in this post are taken from the Quantra course Options Trading Strategies In Python: Advanced. You can preview the concepts taught in this post by clicking on the free preview button and going to Section 6 and Unit 9 of the course.

Note: The links in this tutorial will be accessible only after logging into quantra.quantinsti.com

Note that backtesting results do not guarantee future performance. The presented strategy results are intended solely for educational purposes and should not be interpreted as investment advice.

In this post, we will cover the following topics:

- What is Gamma in Options Trading?

- What is Gamma Scalping?

- How Does Gamma Scalping Work?

- How to manage the transaction costs?

- Gamma Scalping - Example

If you are new to Options trading, the Options Trading Strategies In Python: Basic course would be helpful.

What is Gamma in Options Trading?

Gamma is one of the "Option Greeks" which are key metrics used to assess the risk and potential profit of options positions.

- Delta measures the sensitivity of an option's price to changes in the price of the underlying asset. You can go through this article to learn more about Delta.

- Gamma is the rate of change of delta with respect to the price of the underlying asset. Essentially, gamma measures how much the delta of an option will change as the underlying asset's price changes.

In mathematical terms, if delta is the first derivative of the option's price with respect to the underlying asset, gamma is the second derivative. High gamma indicates that the delta is very sensitive to movements in the underlying asset's price, while low gamma suggests that the delta changes more gradually.

For example, if an option has a delta of 0.5 and a gamma of 0.1, a $1 increase in the underlying asset’s price will increase the delta to 0.6.

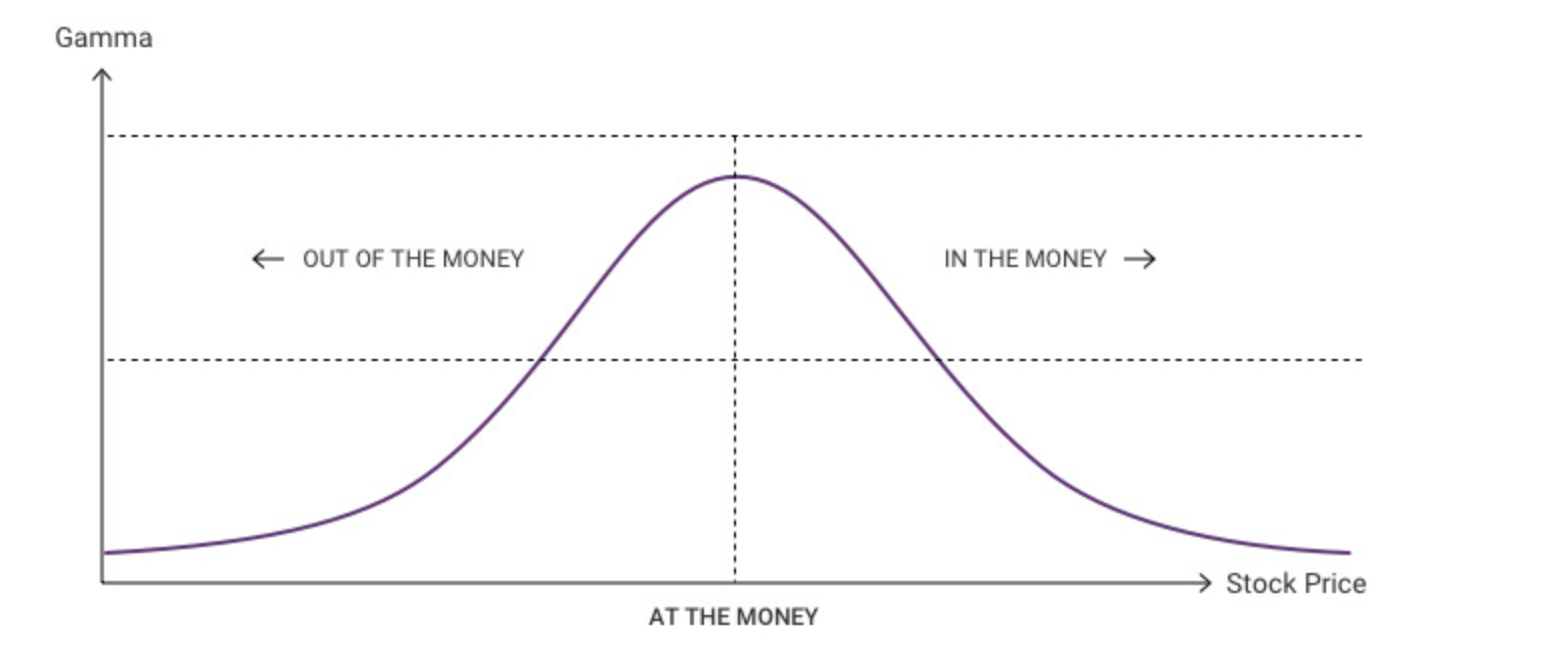

Gamma is highest for at-the-money options and decreases as the option moves further in-the-money or out-of-the-money.

Gamma

What is Gamma Scalping?

Gamma scalping leverages the dynamics of gamma and delta to profit from small price movements in the underlying asset. It involves continuously adjusting the position to remain delta-neutral, meaning that the overall delta of the position is kept close to zero.

The core principle of gamma scalping is to buy low and sell high in the underlying asset or vice versa to capture profits. As the price of the underlying asset moves, the delta of the options changes due to gamma. The trader then buys or sells the underlying asset to counteract the change in delta, thus maintaining a delta-neutral position.

How Does Gamma Scalping Work?

To understand how gamma scalping works, let’s break down the steps involved in this strategy:

- Step 1 - Establishing a Delta-Neutral Position:

The first step in gamma scalping is to establish a delta-neutral position. This means that the total delta of the options and the underlying asset combined is close to zero. For example, if a trader has a call option with a delta of 0.5 and owns 100 shares of the underlying stock, he would need to sell 50 shares to neutralize the delta.

- Step 2 - Monitoring Price Movements:

Once a delta-neutral position is established, the trader continuously monitors the price of the underlying asset. As the price moves, the delta of the options changes because of gamma. The trader then adjusts the position to maintain delta neutrality.

- Step 3 - Adjusting the Position:

When the underlying asset's price increases, the delta of call options increases (or decreases for put options), leading the trader to sell some of the underlying asset to offset the change. Conversely, when the underlying asset's price decreases, the trader buys the underlying asset to counter the decrease in delta. This frequent buying and selling is where the term "scalping" comes from.

The profit in gamma scalping comes from the small price movements in the underlying asset. By buying the underlying asset at lower prices and selling at higher prices, the trader captures small gains. Over time, these small gains accumulate, especially in volatile markets with frequent price swings.

How to manage the transaction costs?

One of the critical factors in gamma scalping is managing transaction costs. Since this strategy involves frequent trading of the underlying asset, high transaction costs can erode the profits. Gamma scalpers often use low-cost trading platforms and carefully manage their trade sizes to minimise costs.

Gamma Scalping - Example

Let’s say a trader has purchased 100 at-the-money call options for a stock currently priced at $100. Suppose the call option has a delta of 0.5 and a gamma of 0.05. Initially, the trader sells 50 shares of the underlying stock to achieve a delta-neutral position.

Scenario 1: The stock price rises to $101. The call option delta increases to 0.55. The trader now needs to sell an additional 5 shares to maintain delta neutrality. Now if the stock price falls back to its previous price, the trader will buy back 5 shares to remain delta neutral. Because the selling price of those 5 additional shares is higher than their purchase price, the trader would capture some profit.

Scenario 2: The stock price falls to $99. The call option delta decreases to 0.45. The trader buys 5 shares of the underlying stock to restore delta neutrality. If the price goes back to $100, the trader can sell those 5 shares at a higher price, thereby capturing a profit.

The table below summarises the possible scenarios:

|

Step |

Stock Price |

Call Delta |

Shares Held |

Action |

Shares Adjusted |

Profit |

|

Initial |

$100 |

0.5 |

-50 |

Sell 50 shares (initial delta-neutral) |

-50 |

$0 |

|

Scenario 1: Price rises to $101 |

||||||

|

1 |

$101 |

0.55 |

-50 |

Sell additional shares |

-5 |

$0 |

|

2 |

$101 |

0.55 |

-55 |

(Total position: -55) |

||

|

3 |

$100 |

0.5 |

-55 |

Buy back shares |

5 |

$1 per share * 5 shares = $5 |

|

Scenario 2: Price falls to $99 |

||||||

|

1 |

$99 |

0.45 |

-50 |

Buy shares |

5 |

$0 |

|

2 |

$99 |

0.45 |

-45 |

(Total position: -45) |

||

|

3 |

$100 |

0.5 |

-45 |

Sell shares |

-5 |

$1 per share * 5 shares = $5 |

In both scenarios, the trader profits from the price movements of the underlying asset due to the changing delta driven by gamma.

We have covered a variation of the Gamma scalping strategy in detail along with the Python code in this unit of the Options Trading Strategies In Python: Advanced course. You need to take a Free Preview of the course by clicking on the green-coloured Free Preview button on the right corner of the screen next to the FAQs tab and go to Section 6 and Unit 9 of the course.