Power of Delta in Options Trading

Here, we will talk about an important Option Greek: Delta. Option Greeks are vital tools for options traders, enabling them to gain deeper insights into their options positions and make more informed decisions. In this Quantra Classroom, we'll break down what Delta is, why it matters, and how you can calculate it and use it for trading options.

All the concepts covered here are taken from the Quantra course on Systematic Options Trading. You can preview the concepts taught in this course by clicking on the free preview button and going to Section 23 and Unit 11 of the course.

Note: The links in this tutorial will be accessible only after logging into quantra.quantinsti.com

What Is Delta and Why Is It Important?

In simple terms, Delta represents an option's price sensitivity to changes in the underlying asset's price. It's like having a compass that points you in the right direction, helping you understand which way your option's value will move when the underlying asset's price changes.

How does Delta behave for call options?

When it comes to call options, Delta takes on a positive value, typically ranging from 0 to 1. This means that as the underlying asset's price goes up, the option's value also rises. It's like knowing that your ice cream will start to melt as the sun gets hotter, indicating a positive correlation between the two.

Call Option Delta

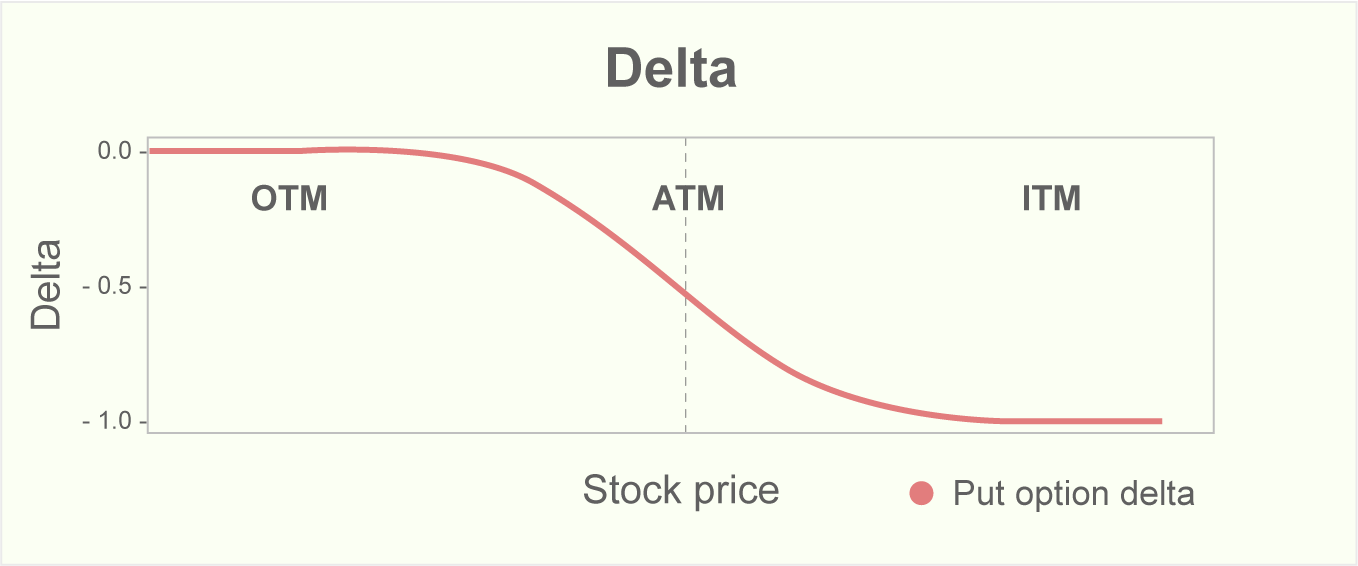

What about put options? How does Delta work for them?

Conversely, Delta is negative for put options and generally ranges from 0 to -1. This implies that as the price of the underlying asset increases, the put option's value moves in the opposite direction, decreasing. Think of doing exercise as the price of the underlying asset and body weight as a delta of the put option. When you engage in regular exercise (similar to a rising stock price in financial markets), your body weight (put option delta) decreases.

Put Option Delta

Is Delta a static value?

Delta is not just a static value; it is more like a slider with a wide range of possibilities, spanning from -1 to 1. For example, a Delta of 0.5 implies that for every $1 increase in the underlying asset's price, your option's value is expected to increase by $0.50. It's analogous to realising that your ice cream gets softer by 50% for every degree it warms up. You are now acquainted with the behaviour of Delta. Next, let's dive into the nuts and bolts of how to calculate Delta.

How to calculate Delta?

Delta can be calculated using the following formula:

Delta = Change in Option Price / Change in Underlying Asset Price

Let's illustrate this with an example:

Suppose a stock XYZ is trading at $100, and the $100 strike call option price is $5. When the price of the stock XYZ changes from $100 to $101, then the $100 strike call price changes from $5 to $5.5. What is the delta of this option?

Delta = Change in Option Price / Change in Underlying Asset Price

Delta = ($5.5 - $5) / ($101 - $100)

Delta = 0.5

In this way, you can calculate the Delta of any option. However, doing this manually for every option can be a tedious process. You can use the mibian Python library to programmatically compute Delta of any option.

How Traders Use Delta?

Traders find Delta invaluable for a variety of reasons. It helps them determine position sizes, manage risk, and develop trading strategies. If you hold a positive view on a stock, one common strategy is to purchase a call option. However, it's essential to be aware that acquiring a call option introduces exposure to various Greeks, such as Vega, Theta, etc, potentially influencing the option's price. To partially mitigate the impact of these other Greeks, you may opt for a bull call spread to capitalise on bullish price movements.

Conversely, if your outlook is bearish, you can either buy a put option or employ a bear put spread.

Nevertheless, prior to implementing any trading strategy, it is crucial to conduct a thorough backtest. This process allows for an evaluation of the strategy's effectiveness, providing insights into its historical performance.

It is important to note that backtesting results do not guarantee future performance. The presented strategy results are intended solely for educational purposes and should not be interpreted as investment advice. A comprehensive evaluation of the strategy across multiple parameters is necessary to assess its effectiveness.

The backtesting of bull call and bear put spread strategies has been covered in detail along with the Python code in this unit of the Systematic Options Trading course. You need to take a Free Preview of the course by clicking on the green-coloured Free Preview button on the right corner of the screen next to the FAQs tab and go to Section 23 and Unit 11 of the course.

What to do next?

- Go to this course

- Click on

- Go through 10-15% of course content

Drop us your comments and queries on the community

IMPORTANT DISCLAIMER: This post is for educational purposes only and is not a solicitation or recommendation to buy or sell any securities. Investing in financial markets involves risks and you should seek the advice of a licensed financial advisor before making any investment decisions. Your investment decisions are solely your responsibility. The information provided is based on publicly available data and our own analysis, and we do not guarantee its accuracy or completeness. By no means is this communication sent as the licensed equity analysts or financial advisors and it should not be construed as professional advice or a recommendation to buy or sell any securities or any other kind of asset.