Trade Options using Forward Volatility

We'll demystify what forward volatility is, explore the mechanics of calculating it, and unveil a dynamic trading strategy that harnesses its power. We used forward volatility to create a volatility trading strategy, and these were the results:

As you can see, the strategy generated a PnL of $25 over a backtesting period of 20 days. It is important to note that backtesting results do not guarantee future performance. The presented strategy results are intended solely for educational purposes and should not be interpreted as investment advice. A comprehensive evaluation of the strategy across multiple parameters is necessary to assess its effectiveness.

All the concepts covered in this post are taken from the Quantra course on Options Trading Strategies In Python: Intermediate You can preview the concepts taught in this course by clicking on the free preview button.

Note: The links in this tutorial will be accessible only after logging into quantra.quantinsti.com

What is Forward Volatility?

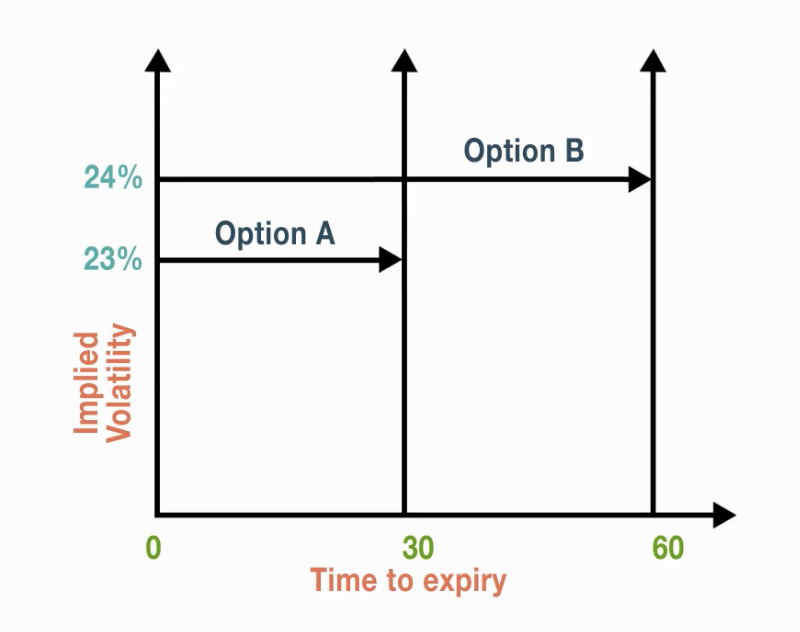

Forward volatility is a measure of the implied volatility (IV) of an option over a period in the future. To understand this with the help of an example, let us consider two options: Option A, with 30 days to expiry and 23% implied volatility, and Option B, with 60 days to expiry and 24% implied volatility. Both Option A and Option B are on the same underlying asset and have the same strike price.

IV vs. Time to Expiry

From the above plot, it is observed that:

For Option B, the implied volatility of 24% can be broken down into two parts; the first part is volatility between 0 and 30 days, which is equal to the implied volatility of Option A. The second part is volatility between 30 and 60 days, which is the volatility for a 30-day forward period, that is, forward volatility.

We can analyse forward volatility and create a trading strategy to benefit from any mispricing of options in the market.

How to Calculate Forward Volatility?

We know that 'variance is additive', using which we will compute the 30-day implied volatility of the two options. The 30-day variance of Option A is calculated using the following steps:

Step 1: Compute the annualised variance, which is the square of the annualised implied volatility.

Annualised Variance = (Annualised IV)2

= (0.23)2

= 0.053

Step 2: Calculate the 1-day variance, which is the annualised variance divided by 365.

1-day variance = Annualised Variance365

= 0.000145

Step 3: Calculate the 30 days variance of Option A by multiplying the 1-day variance of Option A with 30.

30-day variance = 1-day variance 30

= 0.00435

Similarly, the 60-day variance of Option B is square of 24% divided by 365 and then multiplied by 60, which is 0.00947.

Step 4: Next, 30 days forward variance is the difference between the 60-day variance of Option B and the 30-day variance of Option A.

30-day forward variance = 0.00947 - 0.00435

= 0.00512

Step 5: Convert the 30-day forward variance to a 1-day variance.

1-day forward variance = 30-day forward variance30

= 0.00017

Step 6: Calculate the annualised forward variance.

Annualised Forward Variance = 0.00017 365

= 0.0623

Step 7: Compute the forward volatility by taking the square root of the annualised forward variance.

Forward Volatility = Annualised Forward Variance

= 0.2496

= 24.96%

Forward Volatility-based Strategy

The forward volatility of Option B is 24.96%, which seems to be high compared to 23% implied volatility for Option A. If there is no news expected between 0 and 60 days, then the forward volatility of Option B and the implied volatility of Option A should be the same. However, this is not the case. Option A seems to be cheaper than Option B. Thus, we can consider going long in Option A and going short in Option B.

Similarly, we can create a long-short strategy based on the near-month and far-month options. The strategy can be as follows:

- Entry: When forward volatility is more than near-month volatility, go long on the near-month option and short on the far-month option and vice versa. Forward volatility more than near-month volatility indicates that the near-month option is cheaper when compared to the far-month option.

- Exit: The trade is exited at the market close of the same day.

Performance Plot

It is important to note that backtesting results do not guarantee future performance. The presented strategy results are intended solely for educational purposes and should not be interpreted as investment advice. A comprehensive evaluation of the strategy across multiple parameters is necessary to assess its effectiveness.

The strategy discussed above is covered in detail, along with the Python code, in the Options Trading Strategies In Python: Intermediate course.

What to do next?

- Go to this course

- Click on "Free Preview"

- Go through 10-15% of course content

Drop us your comments and queries on the community

IMPORTANT DISCLAIMER: This post is for educational purposes only and is not a solicitation or recommendation to buy or sell any securities. Investing in financial markets involves risks and you should seek the advice of a licensed financial advisor before making any investment decisions. Your investment decisions are solely your responsibility. The information provided is based on publicly available data and our own analysis, and we do not guarantee its accuracy or completeness. By no means is this communication sent as the licensed equity analysts or financial advisors and it should not be construed as professional advice or a recommendation to buy or sell any securities or any other kind of asset.