How to combine the power of value and momentum in your portfolio?

If you’ve ever wondered how to balance stability and growth in your portfolio, we’ve got the right strategy for you. Today we are going to break-down a strategy that lets you combine the power of two factors: Value and Momentum. Apart from these two factors there are other factors such as size and quality too. Factors have often been referred to as “sources of alpha”. With the Quantra course on Factor Investing: Concepts and Strategies you can learn more about factor-based methods of trading.

All the concepts covered in this post are taken from the Quantra course Factor Investing: Concepts and Strategies. You can preview the concepts taught in this post by clicking on the free preview button and going to Section 18 and Unit 1 of the course.

Note: The links in this tutorial will be accessible only after logging into quantra.quantinsti.com

Note that backtesting results do not guarantee future performance. The presented strategy results are intended solely for educational purposes and should not be interpreted as investment advice.

In this post we will cover the following topics:

- Why Combine Value and Momentum?

- How to Combine Value and Momentum

- Analysing the Strategy Performance

The practical implementation of the strategy is done using Python, therefore, if you’re new to Python then you’ll find the free course on Python for Trading: Basic quite helpful.

Why Combine Value and Momentum?

Value and Momentum are two factors that complement each other exceptionally well.

Let’s break down why this combination is so effective:

- Value factor focuses on identifying undervalued stocks—those that the market has overlooked or underappreciated. These stocks have the potential for significant growth once the market realises their true worth.

- Momentum factor, on the other hand, involves buying stocks that have been performing well recently. It capitalises on the continuation of existing trends.

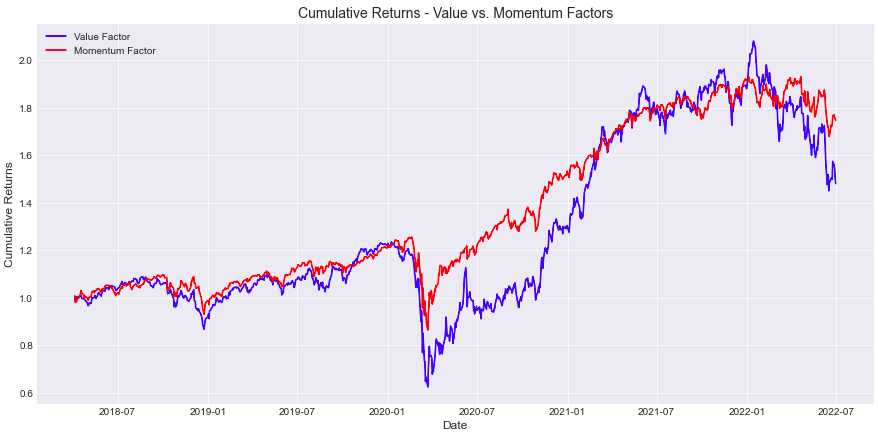

The plot below shows the individual performance of the value and momentum factors:

Here you can see, even though value and momentum factors move in the same direction, the pace at which they move is very different. Blending two factors that have low correlation with each other will likely lead to a more diversified and stable portfolio.

How to Combine Value and Momentum

So, how do you actually combine these two factors?

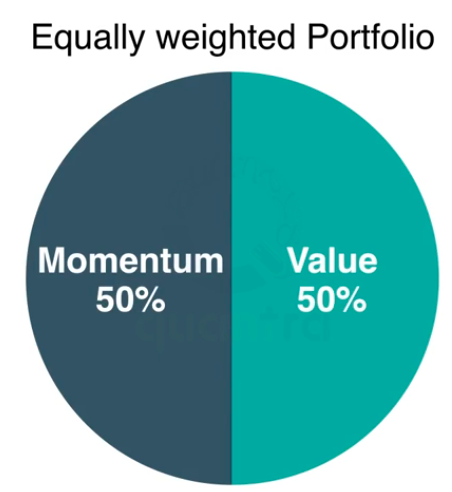

Create an Equally Weighted Portfolio:

- Step 1: Identify stocks based on value metrics and momentum indicators.

- Step 2: Create separate portfolios for each factor.

- Step 3: Allocate 50% of your capital to each portfolio, combining them into a single, equally weighted portfolio.

This approach gives you balanced exposure to both factors. You can also adjust the weights over time to optimise your strategy.

When we combine factors we can compensate for the downsides of one factor by another. The value and momentum factor have low correlation so combining these two factors make a lot of sense. You can create an equally weighted portfolio and you can also adjust these weights to optimise this strategy.

Another way to combine the two factors is to have a value filtered list of stocks and then apply the logic of momentum to trade these stocks.

- Step 1: Start with your universe of stocks and apply a value filter to narrow it down to those that are truly undervalued.

- Step 2: From this select group, apply the momentum factor to take positions on stocks showing strong recent performance.

This method allows you to focus on a smaller, more manageable number of stocks that have both strong value and momentum characteristics.

That's not all! There are more ways to find out which factors should be combined and how you should assign weights to each factor. You can learn more about this in the Factor Investing: Concepts and Strategies course on Quantra.

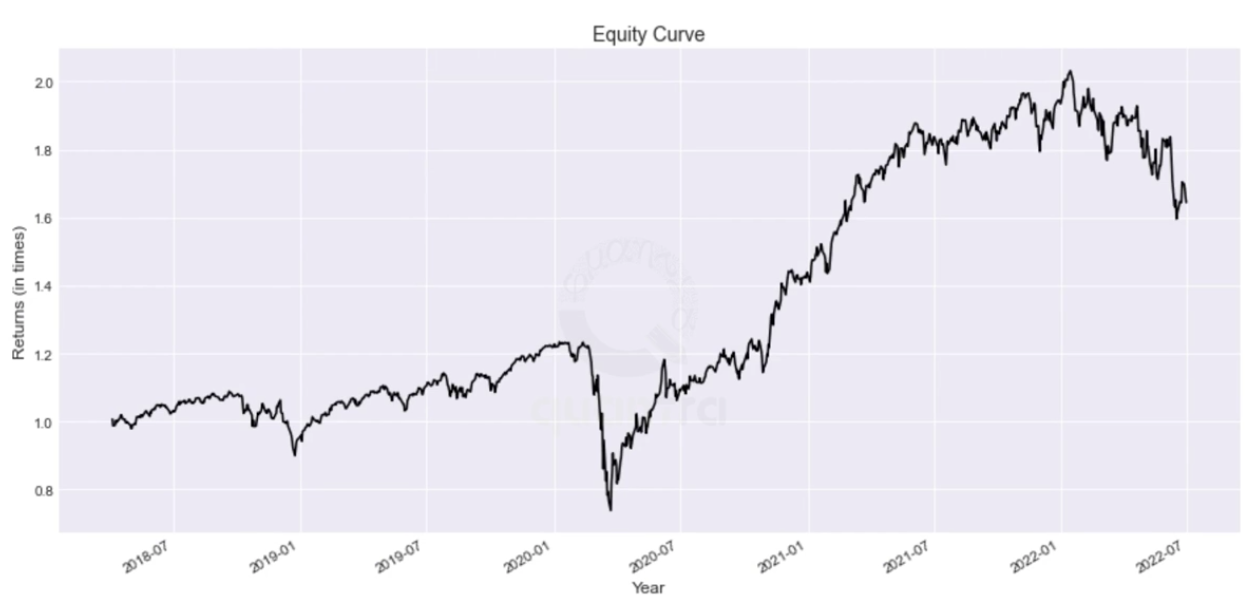

The Results Speak for Themselves

When tested over the period from 2018 to 2022, the combined equally-weighted portfolio resulted in a CAGR of 12.45%. Although it had slightly lower returns as compared to the pure momentum strategy, it did outperform the value strategy. However, it’s important to note that the objective of combining the two factors (value and momentum) was to achieve a more balanced risk-adjusted return, rather than just improving the returns.

This combined strategy not only offers stability during turbulent market conditions but also positions you to capture exciting gains during bullish phases. Research has shown that combining value and momentum factors can lead to better risk-adjusted returns than relying on either factor alone.

Want to see how this works in practice? You can learn more about the implementation of this strategy in Python by accessing Section 18, Unit 5 of the course.

Where to go from here?

Get the code for this strategy and experiment by adjusting the weights of each factor. Observe how these changes impact the overall performance, and then pinpoint the optimal weights that improve the Sharpe ratio.

What to do next?

- Go to this course

- Click on

- Go through 10-15% of course content

- Drop us your comments and queries on the community

IMPORTANT DISCLAIMER: This post is for educational purposes only and is not a solicitation or recommendation to buy or sell any securities. Investing in financial markets involves risks and you should seek the advice of a licensed financial advisor before making any investment decisions. Your investment decisions are solely your responsibility. The information provided is based on publicly available data and our own analysis, and we do not guarantee its accuracy or completeness. By no means is this communication sent as the licensed equity analysts or financial advisors and it should not be construed as professional advice or a recommendation to buy or sell any securities or any other kind of asset.