Short term index reversal

In this topic, we're diving into the fascinating world of equity indices and a smart strategy that can help you make the most of short-term trading opportunities.

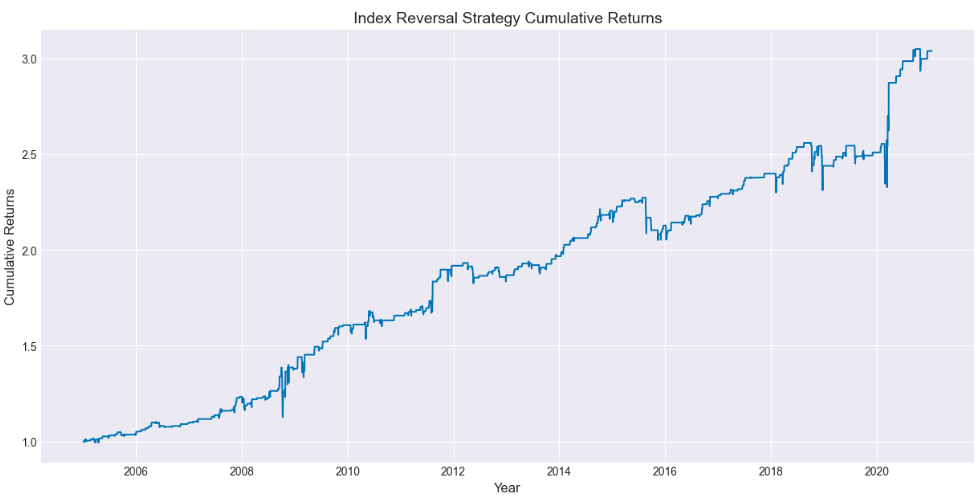

The results of the index reversal strategy are shown below:

As you can see, the strategy has generated an impressive cumulative return of 3x over 16 years starting from 2006. It is important to note that backtesting results do not guarantee future performance. The presented strategy results are intended solely for educational purposes and should not be interpreted as investment advice. A comprehensive evaluation of the strategy across multiple parameters is necessary to assess its effectiveness.

All the concepts covered in this post are taken from Section 4 Unit 1 of the Quantra course on Position Sizing in Trading. You can preview the concepts taught in this course by clicking on the free preview button.

Note: The links in this tutorial will be accessible only after logging into quantra.quantinsti.com

The Power of Equity Indices

Equity indices, such as the S&P 500 or Nasdaq, have long been favoured by investors for a good reason. These indices offer a diverse range of investment opportunities because they include stocks from various sectors. Plus, they're incredibly liquid, making them a go-to choice for short-term trading.

But why should you focus on equity investments, you ask? Well, equities have a historical track record of a rising trajectory, closely linked to economic growth. While bull markets tend to last quite a while, there are also inevitable periods of decline. And that's where our strategy comes into play.

The Pillars of Short-Term Index Reversal

The strategy is built on two solid pillars:

1. Mean Reversion: This is the bread and butter of our approach. In the short term, prices often revert to the mean. When the market experiences a drawdown or heightened volatility, it presents traders with a golden opportunity. Prices dip, and that's when you can buy low and sell high. The short-term reversal strategy bets on the continuation of the long-term uptrend.

2. Overnight Returns Anomaly: Did you know that the US equity premium is largely composed of overnight returns? Surprisingly, overnight performance tends to outshine intraday performance. Now, overnight trading can be a bit expensive due to trading costs and slippages, but here's the kicker – knowledge of this overnight premium can work in your favour.

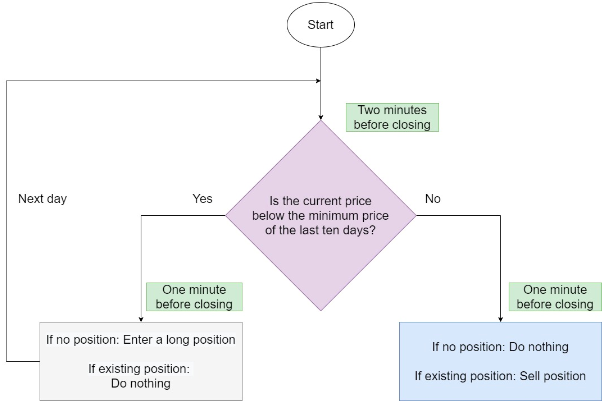

The Trading Setup

Here's how our strategy works:

When you see a series of negative days that push the market to a short-term minimum, it's time to act. We're betting that the negative short-term performance will bounce back – this is mean-reversion in action.

Entry: Overnight performance is typically higher on average. So, what do you do? Enter a trading position just before the market closes. This positions you strategically to capitalize on the overnight gains.

Exit: On the next day, if the current price is not below the minimum price of the last ten days, you can exit your position.

Why Does This Work?

You might be wondering why the market tends to mean revert after a local minimum during the overnight session. Well, research tells us it's because several days of negative performance create market stress. At the local minimum, the equity market usually starts the day with significant negative performance.

As the trading session nears its end, options traders are required to hedge their exposure in the direction of price movement. This creates a temporary intraday momentum, pushing the market further down. The same phenomenon happens with leveraged ETFs. If there's a strong intraday sell-off, managers have to finish the trading day with constant leverage, leading them to rebalance their portfolio in the direction of the negative market movement.

These two reasons create price distortion. The equity index becomes cheaper near the close, and the price corrects itself during the subsequent overnight duration, resulting in a temporary short-term positive drift.

We tested this strategy on the SPY ETF for the period starting from 2005 to 2021 and these were the results:

As you can see, the strategy has generated an impressive cumulative return of 3x over 16 years starting from 2006. It is important to note that backtesting results do not guarantee future performance. The presented strategy results are intended solely for educational purposes and should not be interpreted as investment advice. A comprehensive evaluation of the strategy across multiple parameters is necessary to assess its effectiveness.

Conclusion

So, there you have it – a strategy that combines mean reversion and an understanding of overnight returns to make the most of equity index trading. It's about seizing those short-term opportunities hidden within the market's ebb and flow.

About the Author:

Quantpedia is the encyclopedia/database of quantitative and algorithmic trading strategies. It helps users in processing financial academic research into a more user-friendly form to help anyone who seeks new quantitative trading strategy ideas. You can check out the courses co-authored by Quantpedia here.

What to do next?

- Go to this course

- Click on

- Go through 10-15% of course content

Drop us your comments and queries on the community

IMPORTANT DISCLAIMER: This post is for educational purposes only and is not a solicitation or recommendation to buy or sell any securities. Investing in financial markets involves risks and you should seek the advice of a licensed financial advisor before making any investment decisions. Your investment decisions are solely your responsibility. The information provided is based on publicly available data and our own analysis, and we do not guarantee its accuracy or completeness. By no means is this communication sent as the licensed equity analysts or financial advisors and it should not be construed as professional advice or a recommendation to buy or sell any securities or any other kind of asset.