How to Manage the Risk of an Options Position?

Trading options volatility presents a wealth of diverse trading opportunities. Among these, shorting options is a notable technique. However, many traders approach shorting with caution due to the inherent risk of unlimited losses. Professionals in the field employ various methods to manage and mitigate this risk effectively.

In this post, we will discuss managing the risk of an options position effectively like professionals do!

These techniques are covered extensively in

Advanced Options Volatility Trading: Strategies and Risk Management course of Quantra.

All the concepts covered in this post are taken from the Quantra course Advanced Options Volatility Trading: Strategies and Risk Management. You can preview the concepts taught in this post by clicking on the free preview button and going to Section 24 and Unit 8 of the course.

Note: The links in this tutorial will be accessible only after logging into quantra.quantinsti.com

This post is structured as follows:

- Risk of an options position

- Dollar-Based Risk Management

- Risk Management Using Options Greeks

If you are new to options trading, check out our free course ‘Options Trading Strategies: Basics’.

Risk of an Options Position

Can you trade a stock when you expect the price to not move at all by taking positions in equities or futures? No!

But, options present you a way to trade even when a directional move is not expected!!

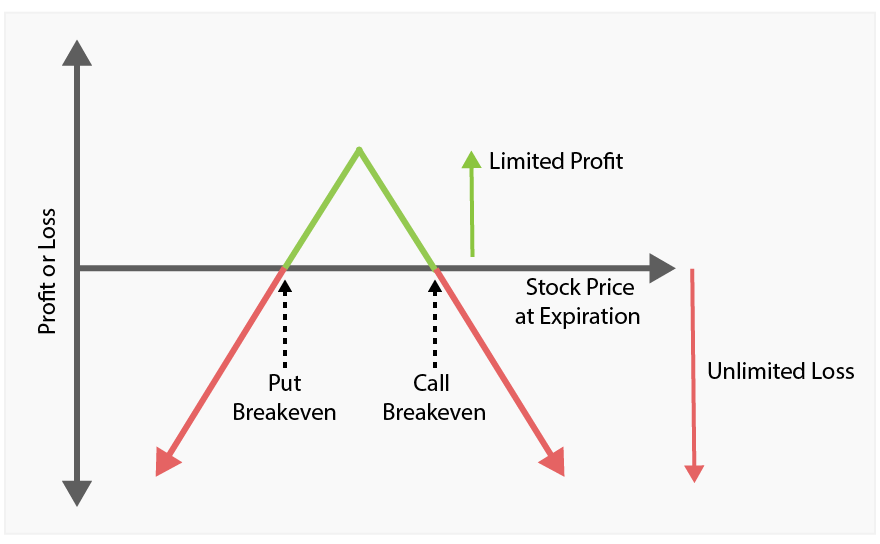

A short straddle is one of the choices for options traders when they expect the underlying asset to remain relatively stable and not exhibit significant price movement in either direction.

A short straddle was created by shorting an atm call and put. But, shorting an options contract would have limited profit and unlimited risk!

As shown by the payoff diagram, the short straddle has the potential for limited profits and unlimited losses.

How to manage the risk of this position?

There are two ways:

- Dollar-based risk management

- Risk management using options Greeks.

Dollar-Based Risk Management

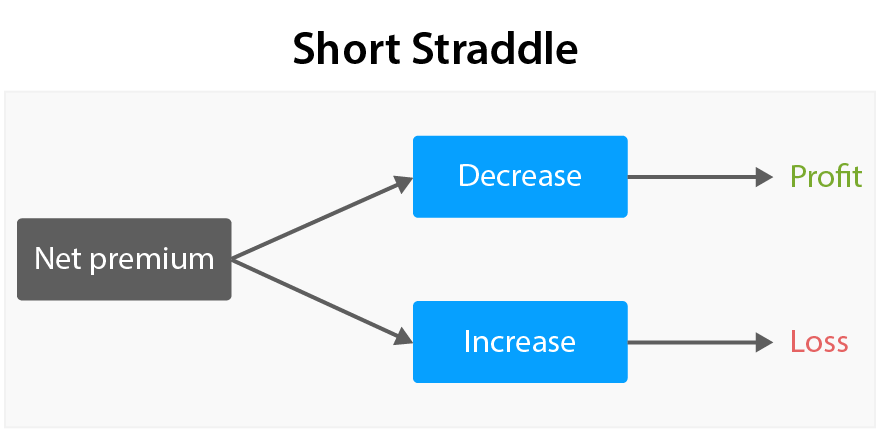

Under the dollar-based risk management technique, the stop-loss and take-profit levels are defined based on the net premium collected.

For example, consider the example of a short straddle opened for SPX options at an ATM strike price of $5000 and collected $20 by shorting a call and $80 by shorting a put, amassing a total net premium collected of $100.

The plan was to buy the straddle back when the net premium declined lower.

Although we expect no movement in price, if the price moved higher or lower significantly, the premiums would spike up and would result in a loss. In fact, as the price increases or decreases, the loss would gradually increase.

So, to limit the loss, we can set a limit called ‘stop-loss’.

For example, if 50% of the net premium is decided as a stop-loss, for our example, the stop loss would be 100 + (0.5*100) = $150.

i.e. the short straddle position will be closed when the net premium increases to $150.

In addition to this, we can also, define a take profit level.

If 50% is set as a take profit level then, for our example, $100 - (0.5X$100) = $50.

I.e. if the net premium falls to $50, then we close the short straddle position and collect the profit of $50. (Profit = Net premium received - Net Premium paid at closing of position)

If you want to implement dollar-based risk management using Python, you can go to section 24 and Unit 8 of the course ‘Advanced Options Volatility Trading: Strategies and Risk Management’.

However, with a dollar-based stop loss, we need to close the short straddle position. But what if we want to hold the position and still manage the loss?

This is what you can do by using the options Greek, Delta for managing risk and the technique is called ‘delta hedging’.

Risk Management Using Options Greeks

A sharp rise or decrease in price results in spice in net premium of a short straddle and results in a loss.

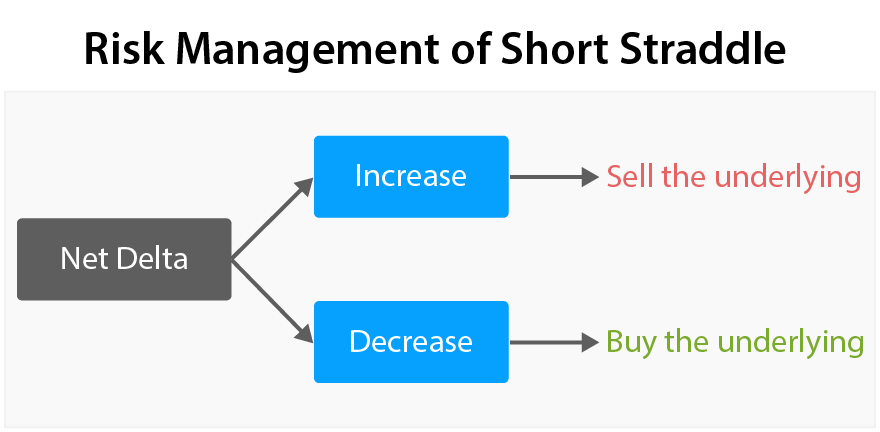

The response of premium with the change of price is explained by the options Greek, Delta. So, limiting the movement of the net Delta of the short straddle would limit the change in premium and control the losses.

In the beginning, when a short straddle is opened, the net delta would be very close to zero but if the net delta increased or decreased, the premium would rise and result in a loss for short straddle.

So, if the delta goes up, we need to open positions in the underlying such that the net Delta declines to 0. Similarly, if the delta goes down, we need to open positions in the underlying to bring up the net delta to 0.

For example, if you consider SPX options for volatility trading, if the short straddle that was opened with a net delta of 0 increased to 0.4, we need to sell 0.4 quantity of underlying asset which is S&P 500 futures.

On the other hand, if the net delta decreases to -0.4, then we need to buy 0.4 quantity of S&P 500 futures to bring back the delta to 0.

However, the delta changes very frequently and if we hedge as frequently as the delta changes, it increases the transaction costs and net PNL will be affected.

Suppose we take a small delta like 0.05 then the frequency of hedging would be very high and the transaction costs would be huge. If the delta threshold is as high as 0.9, then the net delta would never reach the threshold and we would never hedge and never manage the risk. So, we use an optimum threshold such as 0.5. However, it should be noted that the choice of 0.5 for the threshold of Delta is still subjective.

To know more about the implementation of delta hedging, refer to the video in section 29 unit 1 of the course ‘Advanced Options Volatility Trading: Strategies and Risk Management’.

What to do next?

Take a free preview of the newly launched course ‘Advanced Options Volatility Trading: Strategies and Risk Management’. Dive into advanced options volatility concepts with practical applications and focus on risk management. Learn to calculate IV skew, IV rank, and skew rank. Develop entry and exit rules using machine learning and volatility properties.

Enroll in the course and take advantage of a limited-time 75% discount!

IMPORTANT DISCLAIMER: This post is for educational purposes only and is not a solicitation or recommendation to buy or sell any securities. Investing in financial markets involves risks and you should seek the advice of a licensed financial advisor before making any investment decisions. Your investment decisions are solely your responsibility. The information provided is based on publicly available data and our own analysis, and we do not guarantee its accuracy or completeness. By no means is this communication sent as the licensed equity analysts or financial advisors and it should not be construed as professional advice or a recommendation to buy or sell any securities or any other kind of asset.