Capturing Momentum With Machine Learning

Have you ever felt lost trying to catch the momentum in trading? With an ocean of data to analyse, how do you decide what to consider and what to ignore? No worries. Here is machine learning to your rescue. Machine learning algorithms excel at handling large datasets, allowing them to identify patterns and trends that may not be immediately apparent to human traders.

But there are many ML algorithms out there. Which one should you use to capture momentum? Momentum can be classified into positive and negative, so using a classification model would make sense, right? In today’s classroom, we will discuss one such classification model, the XGBoost classifier, in detail.

All the concepts covered in this post are taken from the Quantra course Advanced Momentum Trading: Machine Learning Strategies. You can preview the concepts taught in this classroom by clicking on the free preview button and going to Section 12 and Unit 12 of the course.

Note: The links in this tutorial will be accessible only after logging into quantra.quantinsti.com

Note that backtesting results do not guarantee future performance. The presented strategy results are intended solely for educational purposes and should not be interpreted as investment advice.

In this Quantra Classroom, we will cover the following topics:

- What are boosting or ensemble methods?

- Brief of XGBoost

- How did the need for XGBoost arise?

- Why is XGBoost better than other ML techniques?

- How to use the XGBoost model for trading momentum?

If you are new to machine learning, Python for Machine Learning in Finance course would be helpful.

What are boosting or ensemble methods?

The sequential ensemble methods, also known as “boosting”, creates a sequence of models that attempts to correct the mistakes of the models before them in the sequence.

The first model is built on training data. The second model improves the first model. The third model improves the second, and so on.

In the above image example, the training dataset is passed to Classifier 1.

The yellow background indicates that the classifier predicted negative momentum, and the green background indicates that it predicted positive momentum. The Classifier 1 model incorrectly predicts two instances of negative momentum and one instance of positive momentum. These are highlighted with a circle.

The weights (as shown in the updated datasets) of these incorrectly predicted data points are increased (to a certain extent) and sent to the next classifier i.e. to Classifier 2.

Classifier 2 correctly predicts the two instances of negative momentum which Classifier 1 was not able to predict. But Classifier 2 also makes some other errors. This process continues, and eventually we have a combined final classifier which predicts all the data points correctly.

The classifier models can be added until all the items in the training dataset are predicted correctly or a maximum number of classifier models are added. The optimal maximum number of classifier models to train can be determined using hyperparameter tuning.

Brief of XGBoost

XGBoost, or "eXtreme Gradient Boosting," is like a souped-up version of boosting. It's designed to boost performance by preventing overfitting or learning the training data too well. Its creator, Tianqi Chen, crafted it to be highly effective through careful model design. Just like a high-performance sports car, XGBoost is all about maximising power and efficiency in machine learning.

You can learn more about the XGBoost model by watching the video in the course Advanced Momentum Trading: Machine Learning Strategies.

How did the need for XGBoost arise?

In the evolution of machine learning, we transitioned from manually coding algorithms to teaching machines to learn from data. Initially, problems were categorised into classification (sorting data into categories) and regression (predicting continuous values). However, single models often struggle with certain complexities and variability in data. To overcome this, ensemble learning emerged, leveraging the power of multiple models combined. XGBoost, a form of ensemble learning, became a prominent method for enhancing prediction accuracy by iteratively improving weak models.

Why is XGBoost better than other ML techniques?

The are many reasons for this:

- Spot-On Accuracy: XGBoost nails predictions, finding patterns in financial data with impressive precision.

- Handles Complexity Smoothly: Financial markets are intricate, but XGBoost navigates them effortlessly, understanding nuanced relationships.

- Collaborative Learning: XGBoost teams up with other models to create a powerful ensemble, each contributing its strengths.

- Balances Things Out: Overfitting? No worries. XGBoost keeps it in check so your model stays on track.

Now that you know what XGBoost is and why we are using it, let’s get to the part where we use it in momentum trading.

How to use the XGBoost model for trading momentum?

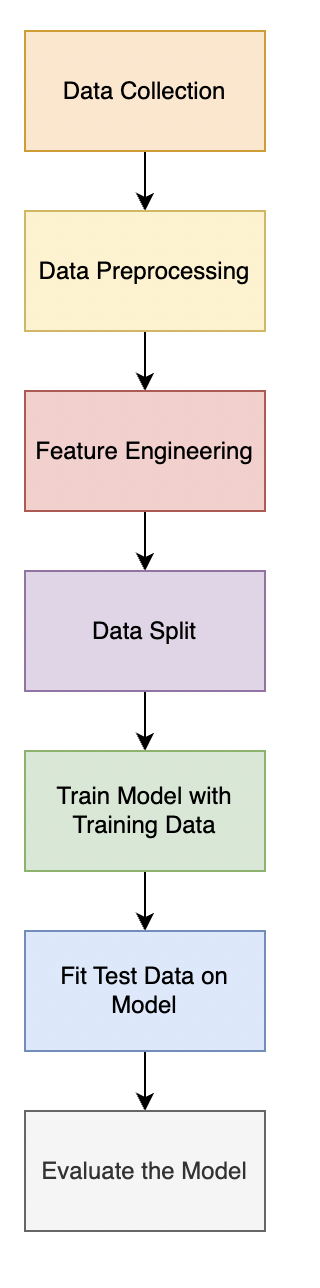

The steps to predict momentum using the XGBoost model are:

Step 1: Data Collection

Accurate and reliable historical market data is crucial for building a robust predictive model. You can gather the price and volume data from trusted sources or APIs, ensuring data quality and accuracy.

Step 2: Data Preprocessing

Data preprocessing ensures that the collected data is clean, consistent, and in a suitable format for the machine learning model. Make sure to correct the errors and handle any missing values in the data before inputting it into the machine-learning model.

Step 3: Feature Engineering

Feature engineering is necessary to extract relevant information from raw data and create meaningful features for the model. You can create relevant features using the price and volume data and pass them to the machine learning model to predict the target variable.

Step 4: Data Split

Splitting the data into training and testing sets allows us to evaluate the model's performance on unseen data. Also, scaling the training data ensures that all features contribute equally to the model fitting process, preventing biases and improving generalisation to new observations. You can use functions such as StandardScaler() to scale the dataset.

Step 5: Train Model with Training Data

Once the data is ready, train the model using the training dataset, enabling it to learn the underlying patterns and relationships in the data

Step 6: Fit Test Data on Model

Using the trained model to make predictions on the test dataset helps evaluate its generalisation ability. By assessing how well the model performs on unseen data, we can validate its effectiveness in real-world scenarios and identify any potential issues or shortcomings.

Step 7: Evaluate the Model

Finally, we will evaluate the model's performance using various metrics like accuracy, precision, recall, and F1-score. This will help us determine the model's strengths and weaknesses and guide further iterations or adjustments to enhance its predictive capability.

We have covered all of these steps in detail, along with the Python implementation in the Advanced Momentum Trading: Machine Learning Strategies course.

The Python code for the implementation of the XGBoost model to predict momentum has been discussed in detail in this unit of the Advanced Momentum Trading: Machine Learning Strategies course. You need to take a Free Preview of the course by clicking on the green-coloured Free Preview button on the right corner of the screen next to the FAQs tab and go to Section 12 and Unit 12 of the course.

What to do next?

- Go to this course

- Click on

- Go through 10-15% of course content

- Drop us your comments and queries on the community

IMPORTANT DISCLAIMER: This post is for educational purposes only and is not a solicitation or recommendation to buy or sell any securities. Investing in financial markets involves risks and you should seek the advice of a licensed financial advisor before making any investment decisions. Your investment decisions are solely your responsibility. The information provided is based on publicly available data and our own analysis, and we do not guarantee its accuracy or completeness. By no means is this communication sent as the licensed equity analysts or financial advisors and it should not be construed as professional advice or a recommendation to buy or sell any securities or any other kind of asset.