Trading the Turn of the Month Effect

In this post, we’ll discuss a fascinating phenomenon known as "The Turn of the Month" effect and create a strategy around it.

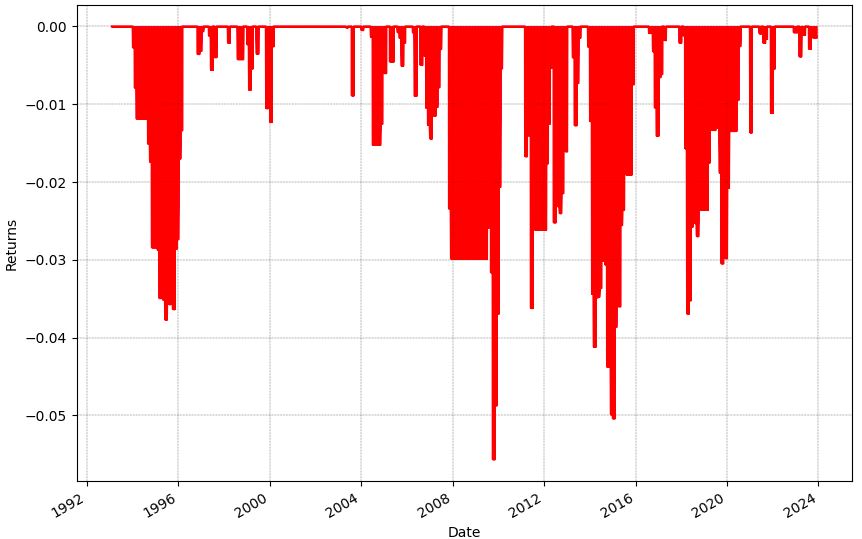

This strategy has been extensively studied and found to be effective not only in the US market but also internationally. We backtested this strategy on the SPY ETF from the period 1993 to 2023 and these were the results:

All the concepts covered in this post are taken from the Quantra course on Event Driven Trading Strategies. You can preview the concepts taught in this course by clicking on the free preview button and going to Section 3 and Unit 6 of the course.

Note: The links in this tutorial will be accessible only after logging into quantra.quantinsti.com

What’s the Strategy?

So, what exactly is this Turn of the Month strategy all about? Well, it's a calendar-based trading approach that revolves around the idea that stock prices tend to rise during the last four days and the first three days of each month.

But why does this strategy work? The secret lies in the regularity of payment dates. Think about it – at the end of the month, investors receive their salaries, dividends, and interest payments. With extra cash in hand, they're eager to invest, which drives up equity prices.

Now, let's get to the most important part – the numbers. Historical data of the SPY ETF, which tracks the S&P 500 index, reveals that the first day of the month tends to be the most profitable. And guess what? This pattern has persisted over the years, delivering consistent returns.

How to trade the turn of the month effect?

Entry Rule: Buy on close at the end of the month

Exit Rule: Sell on close of the first day in the following month.

We backtested this strategy on the SPY ETF and these were the results:

This strategy had a CAGR of 2.87% and the maximum drawdown was 11.97%

Improving the Strategy

But hold on, we're not stopping there! We can enhance this strategy even further to mitigate risks during bear markets. How? By incorporating a trend-following filter, such as the 200-day simple moving average.

This filter acts as a shield, protecting our portfolio during market downturns. The strategy remains inactive if the index price falls below its moving average, ensuring we steer clear of potential losses. In other words, only if the price of the asset is above the 200 period SMA, we will hold our position.

The results speak for themselves. By integrating this trend-following filter, we not only boost our annual returns but also reduce our maximum drawdown, resulting in a more robust performance-to-drawdown ratio.

The CAGR from the enhanced strategy was 2.71% and the maximum drawdown was 5.56%. Even though the CAGR slightly reduced, the maximum drawdown too reduced significantly from 11.97% earlier to 5.56% now.

Conclusion

In essence, the Turn of the Month strategy coupled with a trend-following filter offers a great combination for traders seeking improved returns with minimized risks.

You can also learn more about the implementation of this strategy using Python. All you have to do is take a free preview of Section 4 Unit 2 of the “Event Driven Trading Strategies” course on Quantra.

What to do next?

- Go to this course

- Click on

- Go through 10-15% of course content

Drop us your comments and queries on the community

About the Author of the Course

This course is co-authored by Quantpedia. Quantpedia is the database of quantitative and algorithmic trading strategies. It helps users in processing financial academic research into a more user-friendly form to help anyone who seeks new quantitative trading strategy ideas.

IMPORTANT DISCLAIMER: This email is for educational purposes only and is not a solicitation or recommendation to buy or sell any securities. Investing in financial markets involves risks and you should seek the advice of a licensed financial advisor before making any investment decisions. Your investment decisions are solely your responsibility. The information provided is based on publicly available data and our own analysis, and we do not guarantee its accuracy or completeness. By no means is this communication sent as the licensed equity analysts or financial advisors and it should not be construed as professional advice or a recommendation to buy or sell any securities or any other kind of asset.